THE HOUSING MIRAGE: Canada’s Construction Slowdown Reignites a Crisis of Access

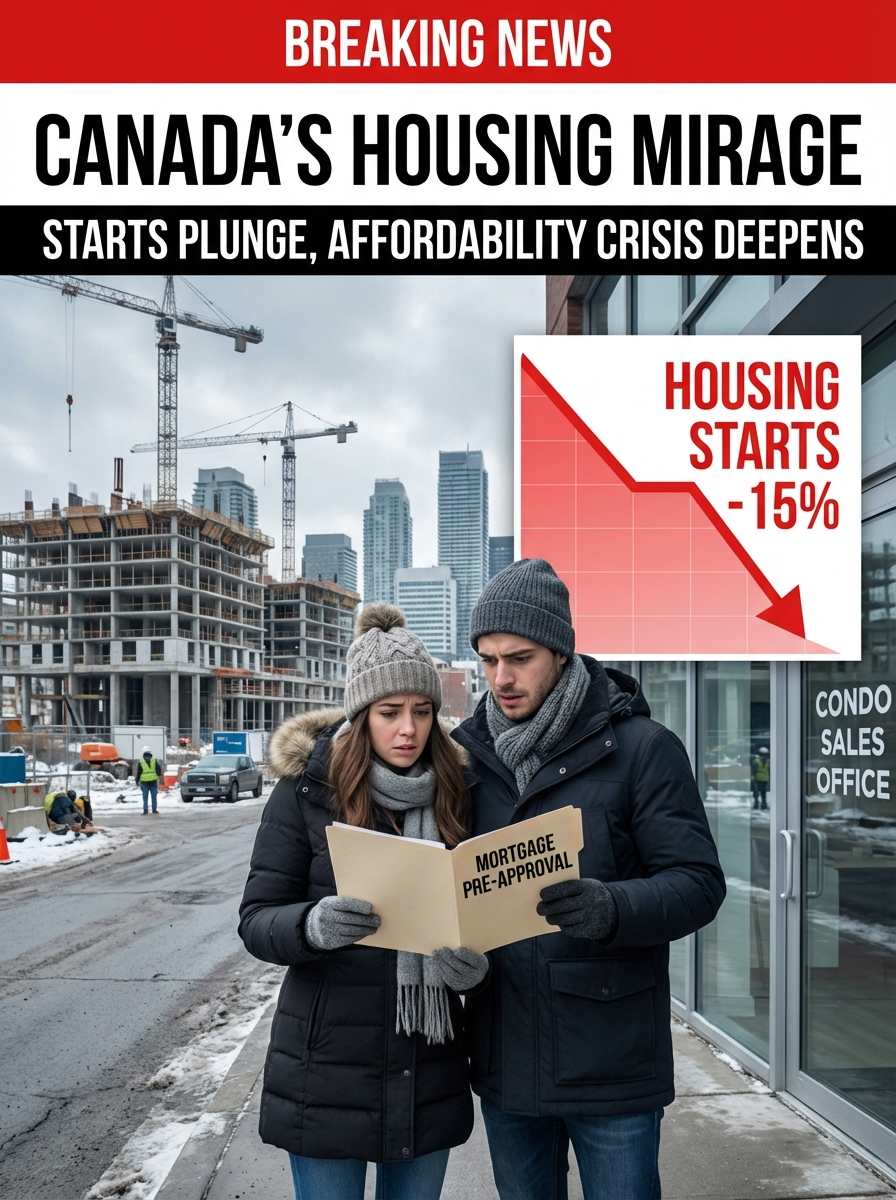

Canada’s housing narrative just took another hit. New data from the Canada Mortgage and Housing Corporation (CMHC) show the seasonally adjusted annual rate of housing starts fell 15% in January 2026, dropping to 238,049 units from 280,668 in December—a steeper decline than economists had expected.

The headline decline is politically explosive because it lands in the middle of a national affordability emergency. Ottawa and provinces have promised to accelerate supply, but monthly volatility is feeding public skepticism about whether policymakers can build fast enough to close the gap between demand and available homes. Reuters reported the January drop was larger than market forecasts, reinforcing concerns that momentum seen late in 2025 may be fading.

Yet the picture is not uniformly bleak. CMHC’s release also says the six-month trend measure declined 3.5%, while actual starts in larger centres (10,000+ population) were up 1% year-over-year in January—evidence that some underlying activity remains resilient despite the monthly pullback.

The contradiction—weak month-over-month data alongside pockets of annual resilience—is exactly why the crisis feels so intractable. Markets need sustained, multi-year expansion in completions, not sporadic spikes. And with borrowing costs, labour constraints, and regional demand imbalances still pressuring builders, every weak print fuels fears that “more supply is coming” may be turning into a recurring political slogan rather than a structural turnaround.

Compounding the tension, broader housing sentiment has softened in key regions. Reuters recently noted weaker Toronto-area sales and persistent uncertainty weighing major household decisions, including home purchases.

For younger Canadians and renters, the practical takeaway is brutal: a one-month 15% drop may be statistical noise in theory, but in an already undersupplied system, it deepens a trust gap in practice. The debate over who is to blame—government execution, financing conditions, municipal bottlenecks, or developer incentives—is intensifying because affordability has become the country’s defining economic stress test. Until starts convert into sustained completions at scale, the “homeownership dream” will continue to feel less like a delayed milestone and more like a disappearing social contract.